By Sean Hanley, Director – Consulting & Advocacy, Pickering Energy Partners

The views expressed by the author are their own and do not represent the views of Energy Workforce & Technology Council.

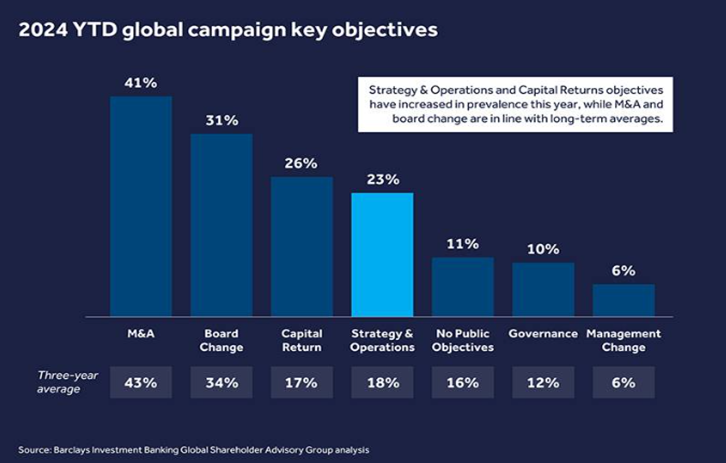

According to a Barclays release through Q3 2024, Activist campaigns were 26% above the four-year average.[1] Activism in the United States is up 22% YoY. 23% of those campaigns are focused on “strategy & operations” which is up from a three-year average of 18%.

Throughout 2023 and 2024, Elliott Investment Management initiated positions in both Phillips 66 and British Petroleum, respectively. Elliott had been vocal with Phillips 66 in pushing for a strategic divestment of its midstream operations and focus on its core refining business.

With Q4 filings due to be filed by February 14th, Elliott communicated its near 5% stake in BP and top 5 position in Phillips 66. Elliott called for Phillips 66 to follow the “Marathon Path.” Marathon Petroleum sold its 3,900-store Speedway gas stations in 2019 for $21 billion following an activist engagement with Elliott. Phillips 66 responded by acquiring $2.2 billion in natural gas pipeline assets last month.

What these engagements are telling the market is that traditional activists are increasing their holdings to forcefully enact change at the board level. The five-year returns of BP and PSX are -4% and +46.9%. By comparison, the S&P 500 and XLE (XOM, CVX, and COP comprise 67% of the index weighting) are up +81.8% and +70.6%, respectively. Therefore, one of the “lowest hanging fruit” datapoints is total shareholder return. Underperformance will attract activists to dig deeper into the company’s strategy and capital deployment profile. Essentially, what do the revenue streams, margin (growth or decline) of those operations, leverage, and return of capital profile look like in comparison to core peers as well as the broader benchmark (S&P 500, S&P 400, Russell 2000, etc). Once the strategic differentiators have been identified the activist will decide if there is opportunity to “unlock” value and generate returns in line with or above peers and the broader market.

Specifically, activists target board seats to enact change. Once board seats have been acquired through the proxy vote, the activist can work to execute on enacting the changes they want to occur. That could range from M&A (acquisition or divestment), an increase or decrease in the dividend or buyback policy, paying down or taking on additional leverage, etc. With the markets at all-time highs, it would be easy to suggest that this wave of activism will continue, and it remains paramount for the Board, Senior Management, and Investor Relations teams to remain aligned on strategy, cash flow generation, capital deployment profile, and return of capital to shareholders. Veering off course in this continual journey can create lagging returns, and ultimately shareholder angst.

The Consulting & Advocacy team at Pickering Energy Partners is collaborating with public and private companies on formulating strategy and executing on those initiatives. Specifically, we are finding success by advising clients to enact three simple principles when engaging on outreach to current or prospective shareholders: “tell a good story,” “don’t embarrass us,” and most importantly “make money.” This generally leads to productive investor meetings, especially with the generalist investors who may not know your story intimately.

[1] 2024 activism boosted by new campaigners and US | Barclays IB

Energy Workforce partner Pickering Energy Partners provides insights on ESG due diligence, disclosures and reporting. Garrett Delk is Associate, Consulting & Advocacy.